Fintech is the short form of Financial Technology. It is a word used to represent a set of new financial technologies aimed to improve and automate the usage and supply of financial services. Fintech brings radical changes in some traditional financial sectors including banking, payments, insurance, personal finance, lending, investments, and wealth management. It’s a multi-billion dollar financial service industry that is changing the economy of the world. India has seen drastic adoption of various types of fintech services in the past couple of years, mostly since 2016, when the government initiated the national demonetization of currency notes. But, in the case of Bangladesh, the country is critically lagging behind on using financial technology. According to ‘Global Fintech Ecosystem Ranking 2021‘, Bangladesh scored 78 out of 83 countries, whereas India ranked 23.

Overview of Financial Technology

Fintech was present in the past since banking cards, ATM machines, and online banking transactions were introduced before 2000. However, in the last two decades, the world has adopted different types of innovative fintech-based services. In reality, financial technology is all around us. When we buy anything using a bank card or mobile payment app, we are actually using fintech. When we make an online payment to buy food, book a hotel, pay utility bills or transfer money to someone, or raise funds online, we are again using fintech. Many people utilize it to conduct different financial activities in considerably more convenient ways than before. Most of the global tech giants have introduced online payment systems in the form of digital wallet services including Apple Pay, G pay, ALIPAY, Amazon Pay, and Samsung Pay. Apart from them, many startups have emerged in the last decades offering innovative technologies to assist consumers and businesses in managing their financial transactions more effectively. According to Statista, from 2010 to 2020, fintech companies received more than $757 BN investment worldwide. In 2019, global fintech companies received the highest investment, amounting to $215.4 billion. In the first half of 2021, they have received $98 billion in funding.

Fintech Landscape in India

India is one of the largest fintech markets in the world. It is also the 2nd highest funded sector of India, after e-commerce. However, in the previous six years, the capital inflow has risen considerably in fintech companies, reaching up to 45%, compared to 20% for e-commerce. It has around 2174 fintech startups as of June 2020. Among them, approximately 67% were introduced in the last 5 years. According to economic times, the total valuation of the Indian fintech industry is estimated at $50-60 billion in 2021 and is expected to grow over 150-160 billion by 2025. Mumbai and Bengaluru became two of the biggest fintech hubs of India.

According to a report of the National Payment Corporation of India (NPCI), 32% of Indian households are using digital payment systems. In the fourth quarter of 2019, for the first time in Indian economic history, card and mobile payments totaled Rs 10.57 lakh crore / $140.69 billion, surpassing ATM withdrawals, which came in at Rs 9.12 lakh crore / $121.39 billion at the same time. That indicates that India is entering into a cashless economy and the era of digital banking.

BaaS or Banking as a Service, has played a significant role in fintech adoption in India. By interacting with traditional banks, fintech, or any non-banking third party via API, BaaS fundamentally helps to bring innovation in banking services. Thus, open-API such as Aadhaar Enabled Payment System (AEPS), Unified Payments Interface (UPI), Mobile Wallets, as well as traditional tools like banking cards, USSD, mobile banking, and POS terminals, have improved the digital banking experience. Digital-only banks, biometric security, blockchain technology, artificial intelligence, neobanking, and innovation on payment systems has become the new trends of the Indian fintech landscape. There are several sub-segments within the Indian fintech ecosystem including digital payments, lending, wealth technology, insurance technology, regulation technology, cyber security, robo advising, and many others.

Digital Payments

Among Indian digital payment-related fintech, Paytm is the largest startup, valuing approximately $25 billion. It is currently offering Paytm wallet, Paytm payments Bank, Paytm Insurance, Paytm Credit Cards, Paytm Postpaid, Paytm Mall, and some other services for merchants and individuals. They have partnered with companies like Ola, Uber, MakeMyTrip, RedBus, and Dominos to better serve their customers. They claimed that almost 50% of merchants hold Paytm payments bank accounts to transact with customers. They have more than 450 million registered users. Phonepe comes next with offering a mobile payment solution and money transfer facility. In 2021, they had over 300 million registered users. According to NPCI, among Indian households who do digital payments, 80% of them use Paytm or Phonepe type apps. Also, there are several other popular platforms for digital wallets like Amazon Pay, Google Pay, BHIM, MobiKwik, etc. On the other hand, Razorpay and Instamojo are quite popular among the payment gateways. In addition, Pine Labs is one of the most popular merchant platforms in India, providing financing and retail transaction technology. Besides that, CRED offers credit card payment facilities to customers as well as rewards on the basis of payments. In addition to these platforms, Airpay, PayU, Citrus, instantpay, Kissht, Billdesk, QuikWallet are some of the notable players in the digital payment industry.

Alternative Lending

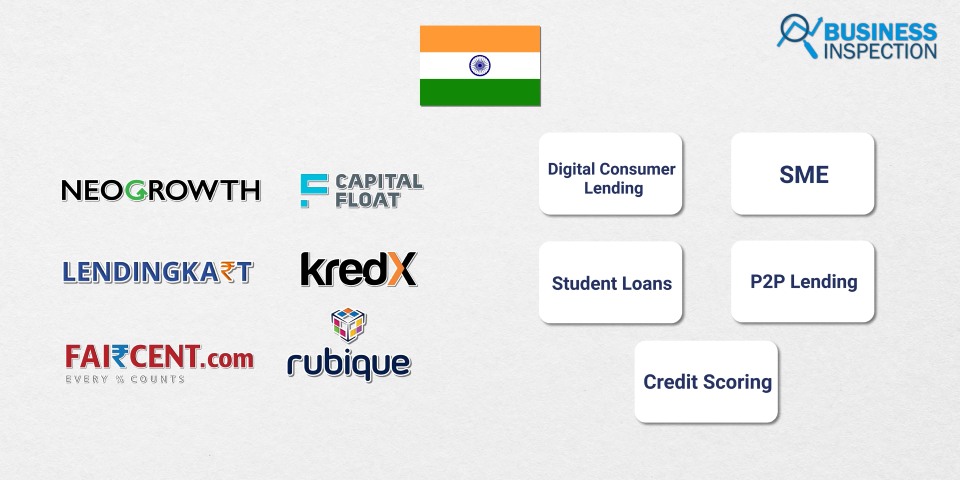

Indian alternative lending fintechs are basically NBFC, offering digital consumer lending, SME/student loans, P2P lending, aggregator, and credit scoring. Lendingkart is a popular name that provides loans to SMEs for working capital. Their fast processing, less documentation, and no requirement for collateral make them appealing to consumers. They have already disbursed more than 100,000 loans in more than 1300 cities and towns of India. Besides that, Capital Float, Ofbusiness, Rubique KredX, Faircent, and NeoGrowth provide SME loans. InCred, Earlysalary, creditmate, ZestMoney, Loantap, MoneyTap, Lazypay, Indialends, Cashe, and paysense are some of the startups that provide personal loans. ‘Shiksha finance’ is an education loan provider app for both institutes and students. KrazyBee is another popular student loan providing platform.

Wealth Technology

Wealth Tech fintechs are offering personal finance management, Robo-advising, investment platform, discount brokering, and many more things. ‘Zerodha’ is India’s largest online brokerage and asset management platform valued at over $2 billion in 2021. The platform offers investment in stocks, derivatives, mutual funds, and so on. ‘ETMONEY’ is another investment app, offering personal finance products including direct mutual fund, SIP investment, ELSS tax saving schemes, national pension scheme, health insurance, life insurance, and credit cards/loans. Besides that, Bankbazaar, Groww, Scripbox, Paisabazaar, Sqrrl Fintech, Upstox are some other popular wealthtech related fintechs.

Insurance Technology

Insurance-related fintechs of India provide online insurance, aggregators, policy management, and claim management. Policybazaar is the most known platform in India. It’s an insurance aggregator that sells different insurance products, provides comparisons, and shares insurance-related knowledge. The company is worth more than $2.4 billion in March 2021. Acko, Toffee Insurance, Coverfox, Digit, Easypolicy are some popular platforms of India in insurance-related fintech.

Fintech Enabler

Fintech Enabler basically helps to uplift the service quality through innovation in the processes of existing traditional financial institutions and fintechs. These kinds of fintech platforms offer various services, mostly for businesses, including on-demand software for customer acquisition and service, E-KYC, anti-money laundering, fraud and compliance management, and risk management, data record, and integration. Some popular names of this type of fintechs of India are Khatabook, CustomerXPs, ClearTax, and many more.

Reason’s Behind the Growth of India’s Fintech Industry

One of the reasons for the growth of India’s fintech industry is the various steps taken by the country’s government. ‘India stack’ is the most influential initiative of the government that helps bring India’s population into a unified digital platform. National Payments Corporation of India (NPCI) developed a Unified Payment Interface (UPI) in order to provide an instant real-time payment system for inter-bank peer-to-peer and person-to-merchant transactions. In the month of August 2021, more than 3.5 billion transactions have been recorded valued over Rs. 639,000 crore under the UPI-based payment system. 249 banks are being operated under the UPI payment system, as of August 2021. Besides that, Immediate Payment Service, National Electronic Funds Transfer (NEFT), Cross-Border Remittances, Bharat QR and Bharat Bill Payment System (BBPS), and National Electronic Toll Collection (NETC) has firmly established India’s payment sector on an upward development path and help straighten the backbone of fintech startups and offer more innovative services.

India’s education system, the growth of the Internet, and the growth of smartphone users have also played a significant role in the growth of the country’s fintech ecosystem. As a result, the country’s startups have received a lot of capital inflows and investments from domestic and foreign venture capital, private equity and institutional investors. Which has further accelerated the growth of the fintech ecosystem. With new payment mechanisms and users developing across regions, this growth is projected to continue in the future. According to Moneycontrol, India is anticipated to contribute 2.2% of the global digital payment industry by 2023.

Fintech Landscape in Bangladesh

Until 2010, Bangladesh’s fintech landscape was mostly limited to debit and credit cards, ATM booths, POS terminals, and to a smaller extent internet banking of the country’s banks. According to a research paper by Mr. Salekul Islam published in Research Gate, Dutch Bangla Bank was the first to introduce Internet banking in Bangladesh in 2003. Despite that. people’s access to banking services was relatively limited. According to the World Bank’s Global Findex Database, Bangladesh’s financial inclusion rate in 2011 was only 32 percent. Bangladesh’s fintech landscape began to change in 2011 when Bangladesh Bank introduced the Bangladesh Electronic Funds Transfer Network (BEFTN) for the first time to improve the adaptability of electronic payment methods and mobile financial services. Then, in 2012, National Payment Switch Bangladesh (NPSB) was introduced to increase interoperability among banks. Agent banking was introduced in 2013 in continuation of MFS. The Digital Financial Services (DFS) Lab was set up in the country in a collaboration between Bangladesh Bank and A2i for the growth of the fintech ecosystem. The adoption of fintech in Bangladesh is constantly increasing by utilizing mobile technology. According to the latest Global Findex Database, Bangladesh’s financial inclusion rate rose to 50% in 2017. According to Gomedici, the total monthly transaction volume processed by financial technology in Bangladesh is approximately $4 billion. According to Tracxn, There are 118 fintech startups in Bangladesh, as of September 2021.

Digital Payments

Bangladesh’s MFS are at the forefront of the country’s digital payment services. MFS began operations in the country in 2011 with the launch of Dutch Bangla Bank Mobile Banking. BRAC Bank launched their own MFS, bKash, in the same year. In addition to these two, several other banks later launched their own MFS, such as Islami Bank’s mCash and UCB Bank’s Upay.

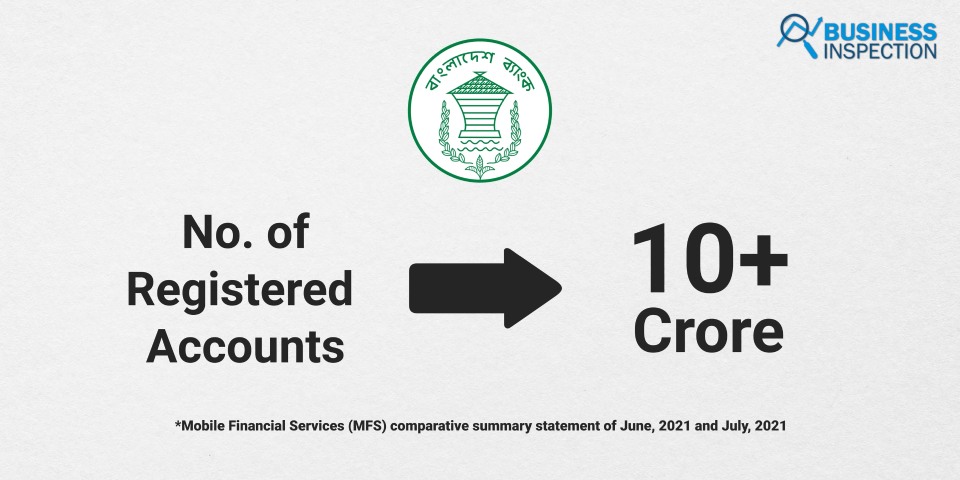

Outside the banks, Nagad – an MFS of the Bangladesh Postal Department, started its journey in 2019. For the first time, the financial services platform has come up with the facility to open an account through ‘Electronic Know Your Customer or E-KYC’ registration process to make it easier for users to open an account. At first, the company was offering the facility of opening an account with a NID card and a user’s picture through the app. Later, with the assistance of mobile network providers, the procedure of opening an account via USSD dial was incorporated into Nagad, with a focus on rural users. Later, other MFSs and banks began to use the Nagad invention to facilitate account opening. Nagad users are currently sending money to any number free of cost, and using the ‘cash out’ function at the lowest rate. Aside from ‘send money’ and ‘cash out’ the country’s MFS’s offer saving schemes as well as online and e-commerce payments, utility bills, university fees, and credit card bill payments. According to Bangladesh Bank, 15 banks are currently operating MFS in Bangladesh. As of July 2021, there are more than 10.27 crore registered MFS accounts in Bangladesh. Apart from MFS, several app based digital wallet services are also operating in Bangladesh. These include Grameenphone’s Gpay, and Robi’s e-wallet providers such as RobiCash, Paywell, iPay, Dmoney, and TopUp.

Apart from MFS, there are several payment gateways for digital payments in Bangladesh. SSLCOMMERZ is the first & leading payment gateway aggregator of Bangladesh. Other renowned payment gateways are Portwallet, which is now operating as Portpos, Lebupay and Surjopay. AamarPay also provides digital wallet services via mobile apps, as well as payment gateway services. On the other hand, the government’s a2i initiative includes a payment gateway called Ekpay. Payment gateways enable customers to make online payments using debit or credit cards, MFS, and Internet banking.

Every year, Bangladesh receives a large amount of remittance. According to Bangladesh Bank, remittances to Bangladesh amounted to more than BDT 210,000 crore in the fiscal year 2020-21. A major amount of these remittances are sent through international money transfer services like Western Union and MoneyGram. Western Union is a well-known brand in Bangladesh’s fintech landscape. However, MoneyGram and Ria Money Transfer are other common methods of sending or receiving money from abroad.

Alternative Lending

Alternative lending is a relatively new phenomenon in Bangladesh. The country has a crowdfunding website named Ekdesh (which is an initiative of a2i), iFarmer, FundSME, and Oporajoy. Essentially, iFarmer is an online crowdfunding platform that connects farmers with investors. FundSME helps entrepreneurs raise funding by connecting them with diverse investor networks, venture capitalists, and business sponsors. Furthermore, Oporajoy is a Bangladeshi crowdfunding platform where anyone can raise funds for personal, charitable, or medical reasons.

Fintech Enabler

There is no company or startup in Bangladesh that offers wealth and insurance technology. However, as a fintech enabler, there are a few marketplace or platforms for locating and comparing a variety of services such as banking, loans, credit cards, and insurance as well as submitting tax returns. Some of the notable companies are SmartKompare, Aamartaka, Banks BD, Phoenix Finance, BDTAX, and digiTAX.

Future Opportunity

Despite the fact that the journey of MFS and online banking started in Bangladesh ten years back, the country’s fintech industry is still growing at a relatively slow rate. One of the causes for this is the people of Bangladesh’s lack of financial and technological knowledge. As a result, Bangladesh has a higher proportion of unbanked people than neighboring nations. The investment for tech adoption and innovation is relatively low in the case of the country’s conventional banks and financial service providers. According to the head of the Bangladesh Association of Software and Information Services (BASIS), the country’s fintech industry is lagging behind due to a lack of financial inclusion and technical adaptation. Apart from that, lack of interoperability between the banking and financial industries at policy level, as well as inadequate rules and restrictions on foreign transactions are some of the causes for the stagnation in Bangladesh’s fintech sector. According to Dhaka Tribune, Bangladesh Bank is taking the step to assure interoperability by the end of 2021. Furthermore, international investment in startups in the country has been expanding in recent years. As a result, it is projected that this industry will continue to expand and flourish in the future.

Leave a Comment