Insurtech refers to the utilization of technology to enhance the efficiency of business processes and models in traditional insurance companies, as well as to provide insurance services to underserved customers. In the Asia Pacific region, approximately 350 insurtech startups have been established, with over 100 operating solely in India. In 2021, 34 insurtech startups in India raised over $800 million in funding. Conversely, in Bangladesh, there has been no adoption of digitization in the insurance sector, and therefore, insurtech startups have not developed in the same manner.

New insurtech companies in Bangladesh essentially aggregate various types of insurance policies from insurance companies and offer them to customers via websites and applications. The insurance penetration rate in Bangladesh is a mere 0.4%, indicating that a large portion of the population does not have access to insurance services. As a result, there is significant potential for traditional insurance companies and insurtech startups in the country to serve the underserved population through digitization of the insurance sector, incorporating new technologies and innovations.

Overview

Upon the conclusion of British colonial rule in 1947, there were 49 insurance companies operating in the region presently known as East Pakistan, which were predominantly administered from West Pakistan. Subsequently, two years following the country’s independence in 1973, all insurance companies within the newly established Bangladesh were terminated in accordance with the Insurance Corporation Act, which was instituted in concordance with the nation’s constitution.

During this time, the government established two insurance entities, specifically the Sadharan Bima Corporation (SBC) and the Jiban Bima Corporation (JBC), with the intent of fulfilling the life insurance and non-life insurance demands of the populace. Nonetheless, in 1984, the 1973 Insurance Corporation Act was nullified to enable private organizations to participate in the industry. As a result of the gradual increase in the number of insurance companies in Bangladesh, a revised amendment to the law was ratified in 1990 with the objective of augmenting the country’s insurance sector.

In 2008, the Ministry of Commerce transferred all responsibility for managing the insurance industry to the Ministry of Finance. Since then, the insurance industry in the country has continued to grow, with the total insurance premium market increasing from Tk 8750 crore in 2012 to Tk 10 (10,383) thousand crore by 2016, representing a 5 percent growth. According to data from a PWC database, there are currently 47 general insurance and 33 life insurance companies operating in Bangladesh. Additionally, Bangladesh Bank reports that there are five types of insurance facilities available in Bangladesh, including Life Insurance, General Insurance, Reinsurance, Micro Insurance, and Takaful or Islamic Insurance. Notably, general insurance covers a range of areas such as health, education, accident, fire, motor, marine, and aviation insurance.

As per a source from the Insurance Development and Regulatory Authority, in 2019, the insurance density per person in Bangladesh was $10.2. In contrast, India’s insurance density during the same period was $78 per person. The premium received from life and general insurance in Bangladesh has exceeded BDT 14,392 crores in 2021. However, the insurance penetration rate in Bangladesh was only 0.4 percent in 2020, whereas India’s penetration rate was over 4.2 percent. Moreover, other countries in the Asia Pacific region, such as Sri Lanka, Indonesia, and Vietnam, have higher insurance penetration rates than Bangladesh, indicating low insurance adoption in Bangladesh.

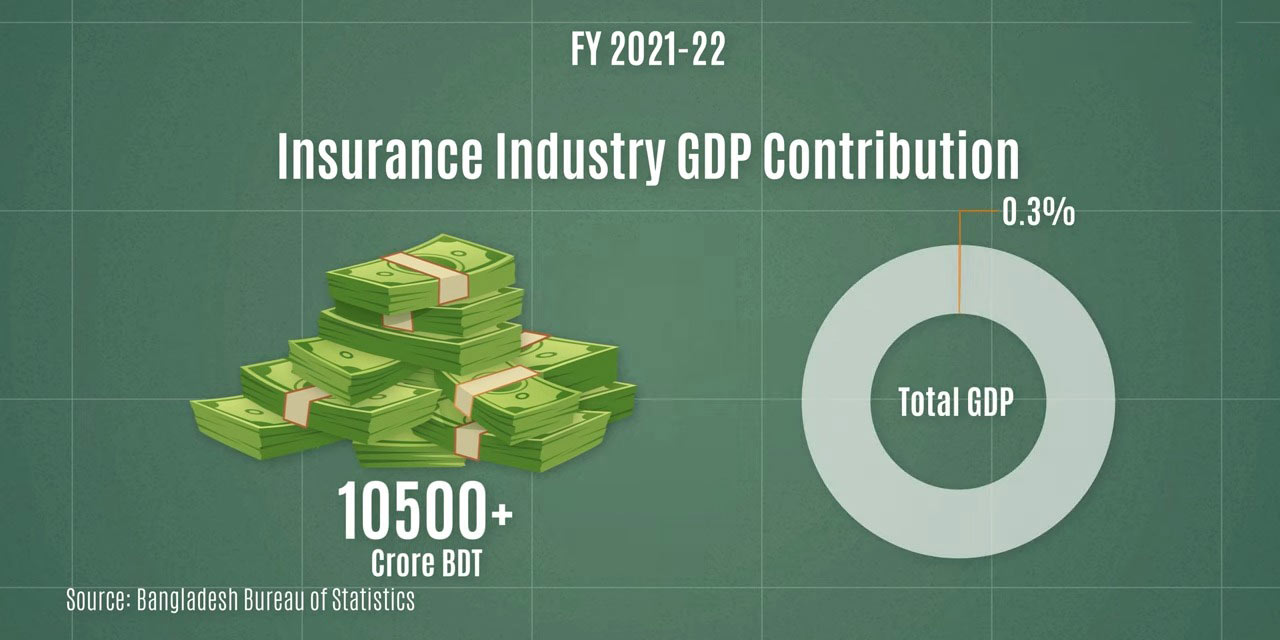

According to data from the Bangladesh Bureau of Statistics, the service sector contributed approximately 2.93 percent to the country’s total GDP in the fiscal year 2021-22. The information and communication sector contributed more than 1 percent, while the transportation sector contributed around 7.47 percent. The insurance industry’s contribution to Bangladesh’s GDP in the fiscal year 2021-22 was more than BDT 10,500 crore, which represents only 0.3 percent of the country’s total GDP.

Technological Adoption

Over the past decade, the financial industry in Bangladesh has experienced significant digitization. The implementation of digital technologies in the banking and mobile financial services (MFS) sectors has resulted in substantial improvements in the financial transaction sector within the country. Despite the impact of digitization on other sectors, there remains a significant deficit in the insurance sector. Currently, none of the insurance services offered by most companies in the country are available online. While the global insurance sector continues to move towards digitization, aiming to enhance customer service and accelerate processing, the utilization of technology in the insurance sector in Bangladesh remains inadequate.

Many industries worldwide have been providing various customer services online or through digital media for a considerable period. In contrast, numerous insurtech start-ups have emerged with the aim of providing insurance coverage to underserved customers in emerging markets and using technological innovation to enhance the efficiency of traditional insurance company business models. In the Asia Pacific region, there are currently a total of 335 insurtech start-ups, with 110 in India alone. India and China are responsible for 78 percent of total insurtech investment in the region. Furthermore, according to the Inc42 State of Indian Fintech Report Q2 2022, India’s insurtech industry is expected to grow at a CAGR of 57 percent by 2025, reaching a $339 billion market. In 2021, 34 insurtech start-ups in India raised a total of $822 million.

In terms of fundraising, PolicyBazaar is one of the top insurtechs in India, having raised more than $700 million since its inception. Policybazaar is basically an insurance broker that aggregates the policies available in the Indian market and allows users to compare and buy through their platform. The company has served more than 50 insurance companies in India including life, health, motor vehicle, and various types of insurance through its own platform to about 9 million customers. Apart from providing various policy information, comparing, buying, and renewing facilities, PolicyBazaar also helps users with policy claims taken through the platform. And all this is done by the company digitally, i.e. by collecting information from users through its own web platform or mobile app. On the other hand, Digit Insurance, another one of the top insurtech companies in India, raised about $600 million and is basically a general insurance company. But the difference between Digit Insurance and other general insurance companies is that, in addition to offering various innovative insurance policies online, this company offers self-inspection and pre-inspection facilities for customers through smartphones, along with a paperless process for buying and claiming insurance policies. Making the process faster and more convenient.

Based on The Daily Star, there are currently approximately 10 companies operating in Bangladesh that offer digital insurance services in collaboration with various insurance companies. Although insurance premiums can already be deposited through a variety of mobile financial services (MFS) and internet banking options, no institution has yet implemented fully digital or technology-based insurance services. Metlife Insurance is the sole insurance company in the country that provides its insurance-related services online. In addition, several aggregator platforms such as BIMAFY, MILVIK, and Surokkha are partnering with various insurance companies to offer their policies to customers through their platforms.

Consumer Mindset

Nearly all banks in Bangladesh currently offer online transaction facilities, such as City, BRAC, EBL, MTB, DBBL, and Standard Chartered, which provide a range of services for their customers, including mobile apps, online account opening, and deposit and fixed deposit services. The use of these digital services is increasing among the educated and upper classes, including the tech-savvy youth of the country. In addition to banking services, this customer segment is also engaging in limited online activities such as investing and trading in the stock market.

Several sectors of Bangladesh, such as education, ride-sharing, food delivery, grocery, e-commerce, courier services, and truck rental, have started various tech-based start-up activities, and these have been well-received by people of different classes and professions. However, the adoption of technology in the insurance sector remains limited. Although some banks in the country offer customers the option to integrate insurance premium payments, most insurance payments are still made through mobile financial services.

Given the widespread adoption of technology in other sectors and among the common people of Bangladesh, it is expected that people would be interested in taking out different insurance policies if digital services were made available for comparing policies based on different criteria, document requirements, and payment options. Therefore, if an app or website-based service is developed for insurance policy comparison and other related services, it would become more convenient for consumers in the country to access insurance services.

Challenges

Lack of Faith

The people of Bangladesh have held a negative perception towards insurance for a considerable duration of time. This is due to their experiences with fraudulent activities that led to significant losses. The reluctance, negligence, harassment, and non-payment of insurance claims have been the primary causes behind such occurrences. As a result, the people have developed a sense of distrust towards insurance companies, and this skepticism persists to this day, with incidents of fraudulent practices still occurring in various insurance companies in the country.

As the insurtech industry is gradually emerging in Bangladesh, the majority of the players are aggregators. However, the negative attitude of the people towards insurance companies can pose a significant challenge to the growth and success of the insurtech companies.

Lack of Awareness

Despite the growing economy, the insurance sector only contributes 0.3 (0.28) percent to the country’s GDP, mainly due to the lack of awareness among the populace. Many people in the country remain without insurance coverage as a result of inadequate understanding of the insurance sector. The majority of the population does not possess proper knowledge about insurance, its advantages, the available policies, the ideal duration of coverage, the return policies, and other relevant information. Additionally, being a Muslim-majority country, a significant number of individuals do not express interest in insurance.

Lack of Government Supervision

Currently, Bangladesh does not have any policies in place to facilitate the digitization of its insurance sector or the emergence of new insurtech startups or institutions. Consequently, insurtech companies in the country have yet to embark on any digitization initiatives. Given the low level of insurance adoption in Bangladesh, it is imperative for the government to establish guidelines and regulations aimed at promoting digitization in the sector. This would encourage insurance service providers in the country to pursue digitization and remain enthusiastic about the development of new insurtech ventures.

Potential of Insurtech

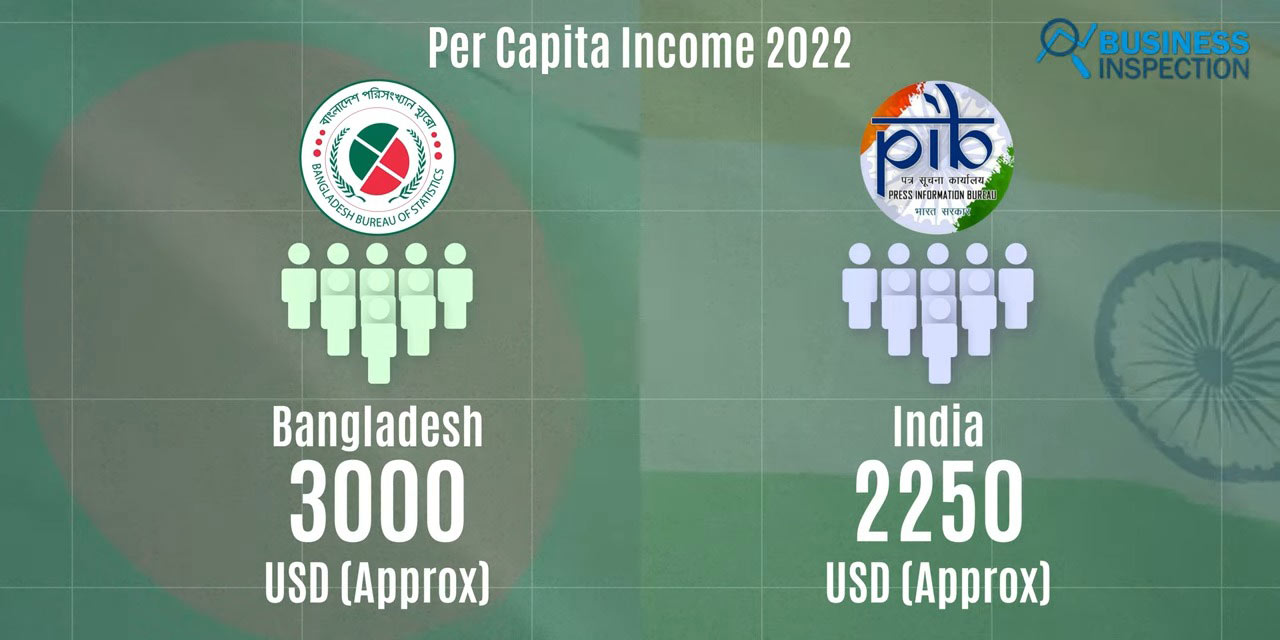

In 2022, the Bangladesh Bureau of Statistics reported that the per capita income of the country’s citizens was approximately $3,000, while the Press Information Bureau of India disclosed that the per capita income of India’s people was about $2,250. Based on this information, it can be inferred that the people of Bangladesh have experienced an increase in their ability to afford insurance compared to previous years. However, in contrast to this development, the average expenditure on insurance in Bangladesh is only 10 dollars, while the average spending on insurance in India is over 78 dollars. This suggests that even though the people of Bangladesh have the financial means to afford insurance, they are not availing themselves of insurance services.

According to the Financial Institutions Division, out of a population of approximately 170 million, only 6 million people in Bangladesh are currently under insurance coverage, indicating that the majority of the population remains without insurance. This highlights the potential for insurtech start-ups and other insurance companies in Bangladesh to capture a significant share of the market through the adoption of technology.

In 2012, the number of internet users in Bangladesh amounted to only 30 million. However, in the last decade, this figure has risen to more than 125 million. The growth in internet users has been accompanied by a corresponding growth in mobile financial service providers in the country. As of 2022, there are more than 180 million registered MFS accounts in Bangladesh. Since their launch in 2011, MFSs such as Bikash, Nagad, and Rocket have introduced mobile apps at various locations including showrooms, super shops, schools, colleges, universities, and have integrated utility services such as electricity, gas, water, and credit cards, as well as services like cable TV and internet service billing into their mobile apps.

The adoption of MFS has been facilitated by the extensive agent network of organizations across the country and such integration. Additionally, various commercial banks and financial institutes in Bangladesh are already offering financial services through mobile apps. Most banks in the country allow customers to open bank accounts using e-KYC through the app, transfer money, engage in e-commerce, and pay bills via the app. As a result, transactions through apps and the internet are constantly increasing in the banking sector.

Insurtech companies operating in Bangladesh should prioritize increasing the awareness of insurance policies among the general public, improving the process of documentation and verification of policies, facilitating the purchase of policies through the use of technology, as well as streamlining the premium payment and settlement of insurance claims. Currently, the process of filing insurance claims in Bangladesh is cumbersome and inconvenient for customers.

In contrast, in Western countries, customers can easily submit evidence such as photographs, videos, and insurance details via email or other digital means in the event of an accident, which makes claiming insurance much more straightforward and convenient. The popularity of motor vehicle insurance in developed countries can be attributed to such ease and convenience. In contrast, motor vehicle insurance is not widespread in Bangladesh, but if insurtech companies can leverage technology to make taking insurance and filing claims more convenient, the future of the insurtech industry in Bangladesh looks very promising.

Moreover, in the healthcare industry, insurance is essential to accessing most health-related services worldwide. However, insurance is not prevalent in the healthcare sector of Bangladesh. As the healthcare market in Bangladesh is growing rapidly, the insurtech industry can tap into this sector by offering health insurance policies to customers seeking medical services. Insurtech companies can make the process of purchasing health insurance policies and filing claims more convenient for customers by providing apps or websites in hospitals. By doing so, the insurtech industry can ensure that customers receive quality medical services and streamline the process of filing insurance claims, making it a lucrative sector for the insurtech industry.

In addition to simplifying the processes of policy purchase, premium payment, and policy claims, the integration of insurance policy purchases through apps or websites should also be considered when purchasing other services or products. For instance, when buying a Samsung smartphone from Peekaboo’s or Samsung’s national distributor Excel’s website, customers have the option to purchase insurance coverage for the mobile display or the entire mobile. Similarly, iFarmer, the country’s top agritech company, offers the option of integrating insurance for investors’ investments with the app. In other words, insurance policies should be easily and conveniently provided through merchant end apps or websites for a variety of products, including electronics such as phones, TVs, and fridges, as well as cars, which can help increase the adoption of insurance in the country.

With the increasing use of motorbikes in the country, insurance purchasing options can be integrated with customer purchase information from showrooms. For ride-sharing drivers, insurance policy purchases, premium payments, and claim options can be integrated into the app, and such options can be extended not only for motorbikes or private cars but also for commercial vehicles through apps like Truck Lagbe or GIM.

In addition, the country’s private sector and production-based industries have experienced significant growth in the last decade, creating a lot of employment opportunities. Innovative insurance products tailored for employees working in these sectors can be introduced in the market. Furthermore, travel insurance services can be offered with the help of TravelTechs such as ShareTrip or GoZayaan. In conclusion, if technology can simplify processes such as policy buying, premium payment, and policy claims, Insurtechs in the country will be able to make significant changes to the insurance sector.

Leave a Comment